On 7 April 2016 the Commission adopted an Action Plan on VAT – Towards a single EU VAT area

The Action Plan sets out immediate and urgent actions to tackle the VAT gap and adapt the VAT system to the digital economy and the needs of SMEs.

It also provides clear orientations towards a robust single European VAT area in relation to the definitive VAT system for cross-border supplies and proposes options for a modernised policy on EU rules governing VAT rates.

Key actions

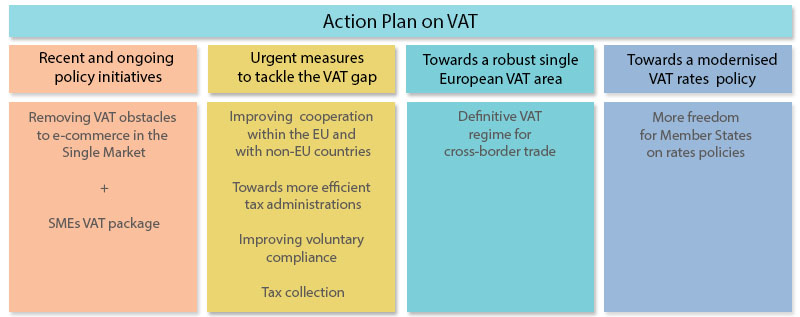

Recent and ongoing policy initiatives

Removing VAT obstacles to e-commerce in the single Market

The current VAT system for cross-border e-commerce is complex and costly for Member States and business alike. The Commission will, as part of its Digital Single Market strategy, present a legislative proposal by the end of 2016 to modernise and simplify VAT for cross-border e-commerce by:

- Extending the current One Stop Shop concept to all cross-border e-commerce, including distance sales,

- Introducing common EU-wide simplifications measures to help small start-up e-commerce businesses,

- Streamlining audits in this sector (home country audits), and Removing the VAT exemption for the importation of small consignments from suppliers in third countries.

SMEs VAT package

SMEs bear proportionally higher VAT compliance costs than large businesses due to the complexity and fragmentation of the EU VAT system. Further to the new Single Market Strategy, the Commission is preparing a comprehensive simplification package for SMEs that will seek to create an environment that is conducive to their growth and favourable to cross-border trade.

In particular, the special scheme for small enterprises will be subject to review. This proposal will be presented by the end of 2017.

Urgent measures to tackle the VAT Gap

The ’VAT gap’ between expected revenue and revenue actually collected by national authorities is estimated at around EUR 170 billion, which equates to 15.2% of revenue loss. This calls for urgent action on several fronts:

- Improving cooperation within the EU and with non-EU countries

- Towards more efficient tax administrations

- Improving voluntary compliance

- Tax collection

20 measures to tackle the VAT gap

In 2016, the Commission will present:

- Measures to improve cooperation between tax administrations including from non-EU countries and with customs and law enforcement bodies and to strengthen tax administrations' capacity for a more efficient fight against fraud.

- Evaluation report of the Directive on the mutual assistance for the recovery of tax debts

In 2017, the Commission will present:

Proposal to enhance VAT administrative cooperation and Eurofisc

Towards a robust single European VAT area

Definitive VAT regime for cross-border trade

The present VAT system, which has been in place since 1993 and was supposed to be transitional, splits every cross-border transaction into an exempted cross-border supply and a taxable cross-border acquisition. It is like a customs system, but lacks equivalent controls and is therefore the root of cross-border fraud.

It is also complex for the growing number of businesses operating cross-border and leaves the door open to fraud: domestic and cross-border transactions are treated differently and goods or services can be bought free of VAT within the Single Market.

To this end, the Commission will present in 2017 a legislative proposal for a definitive VAT system for cross-border trade. This definitive VAT system will be based on the principle of taxation in the country of destination of the goods, as agreed by the European Parliament and the Council.

The Commission considers that in the definitive VAT system, the taxation rules according to which the supplier of goods collects VAT from his customer should be extended to cross-border transactions.

This will ensure consistent treatment of domestic and cross-border supplies along the entire chain of a production and distribution, and re-establish the basic features of the VAT in cross-border trade i.e. the fractionated payments system with its self-policing character.

Infographics

Presidency paper – VAT-fraud

Opinion of the VAT expert group on the action plan on VAT – creating a definitive regime 20 may 2016

The VEG welcomes the initiative of the EU Commission to further explore possible options for implementing the destination principle in B2B cross-border trade in order to ensure a level playing field between EU cross-border and domestic transactions and at the same time tackling the problem of VAT fraud.

The VEG calls upon all stakeholders – Member States, Commission and business to:

- make effective use of existing measures to tackle VAT fraud in the short term. In particular, Member States and the Commission should make increased efforts to improve the efficiency of and international cooperation between national tax administrations;

- cooperate to tackle and resolve the problem of VAT Fraud in the EU VAT system in a coordinated approach that is fully compatible with the requirements of the Single Market. Such approach should incorporate a comprehensive impact assessment of the costs, benefits and effectiveness of the measures proposed for all stakeholders; and

- actively, timely and efficiently work together in order do create a robust,fairand efficient destination based definitive system for the Single European VAT Area.

The Action Plan launched by the EU Commission calls for urgent action on devising an EU wide definitive VAT regime in consultation with all stakeholders in accordance with the Commission’s Better Regulation guidelines.

Any Member State specific approaches, such as a generalised reverse charge system, even on an experimental and national basis, would put at risk the development of a coherent, harmonized and fraud proof VAT system for all Member States and stakeholders.

Any such uncoordinated standalone measures adopted by Member States would shift focus from the overriding objective of putting in place a definitive regime at the earliest opportunity.

It would create additional distortions within the internal market and thereby also increase opportunities for fraud.

We urge the Commission and Member States to abstain from supporting such Member State specific approaches and to work together with all stakeholders in devising a definitive VAT system.

We as VEG remain highly committed to further share our VAT technical and practical expertise and experience throughout the whole process of this initiative.

We remain at the EU Commission ́s and Member States ́ disposal to provide active support.

VAT fraud spotted within days - No substantial change at tax authorities

Data system tested for Benelux countries will be rolled out within 1 year according to current EU Chairman Wiebes. The big data analysis started 1.5 years ago in the Benelux and that participation has already increased to 10 EU Member States amongs others Romania that faces substantial VAT fraud. (source: FD - in Dutch).

Austria applies for pilot project against VAT fraud

Pilot project for "reverse charging" on intercompany business

Finance Minister Dr. Hans Jörg Schelling aims in future to take stronger action against VAT fraud. The Finance Minister's plan would be to transfer settlement of value added tax to the "reverse charge" system, which is less vulnerable to fraud.

Since value added tax is subject to EU law, the European Commission must consent to any system change. Finance Minister Schelling will file the relevant application at the meeting of euro Finance Ministers. "As a result of organised carousel fraud, across Europe, EUR 17 billion is lost in tax revenue; in Austria alone, the figure is around EUR 500 million. This cannot be allowed to continue," stressed Schelling.

The core of the plan would be reversal of value added tax liability ("reverse charging"). At present, fraudsters are able to send goods in a circuit between several countries.

The sales tax is then invoiced by the supplier and the recipient of the goods can obtain reimbursement of the money from the tax office by way of input tax deduction. However, the supplier ends up not paying the tax to the tax authority and files for bankruptcy.

As a result, the revenue authority ends up bearing the costs. Through the "reverse charge" system, this problem would be solved, since the tax liability passes to the recipient of the goods and input tax deduction no longer applies.

"We have already converted to the reverse charge system several sectors that are particularly vulnerable to fraud. However, this is not enough, since the various EU countries are adopting different approaches in this regard. What we don't want is for a hotchpotch to emerge," adds Schelling. "The aim is therefore now to launch a pilot project and to transfer all business between companies to the reverse charge process,". Schelling now hopes to get the green light from the Commission for the field trial.

Source: Schelling applies for pilot project against VAT fraud

Roadmap to manage VAT fraud and reduce liabilities

Benchmark survey on tax

Chapters of GITM

- VAT fraud

- European Commission - VAT lost across the EU is estimated at €168 billion

- New EU Study confirms billions lost in VAT gap

- Quick reaction mechanism

- What is tax avoidance?

- Tax fraud: commission looks at how VAT collection and administrative cooperation can be improved

- Study to quantify and analyse the VAT gap in the EU-27 Member States 2012